While there is strong evidence to suggest that markets move through long bullish periods followed by long bearish periods, and that these cycles tend to last about 17 years on average, it is difficult to identify with precision the beginning and end of any long cycle. For this reason, investors should adopt a strategy that has the potential to perform equally well when markets go sideways or down, as this condition is not just likely, but virtually inevitable over most investors' investment horizons.

Timing systems should be stress-tested in all types of market environments before we can conclude that they are broadly effective. Many systems are uniquely effective in certain markets and under certain conditions, but break down in other market situations. As it is impossible to predict what kind of markets investors will face in the future, we don't want to apply a system that is only effective in certain types of markets.

Timing Strategies Work in Bear Market Periods

CXO Advisory Group recently published a study of timing systems and their effectiveness over the 1999 - 2009 period. This period was chosen deliberately, as during this period a buy and hold strategy of U.S. stocks actually lost 0.7% annually (see Chart 1.). During this period, the authors show that applying a simple coin-flip strategy, where at the end of each month a coin is flipped to decide whether to own stocks for the next month, or sell stocks and be in cash, would have beat the market 85% of the time. While no volatility statistic is cited in the study, the authors do mention that volatility experienced by coin flippers is lower than the volatility of buy and hold.

Chart 1. S&P 500 Total Returns Dec. 31, 1999 through Dec 31, 2009

Source: TradingBlox, Shiller (2011)

The CXO study tested 5 simple systems (plus Buy and Hold), per their report:

- Buy and Hold: Buy and hold S&P 500 stocks (as a benchmark).

- EW SPY-Cash: Hold equal amounts of SPY and cash, rebalancing monthly.

- 10-Month SMA: Hold SPY (cash) when the monthly close of the S&P 500 Index is above (below) its 10-month simple moving average (SMA).

- 6-1 Momentum: Hold SPY (cash) when the past 6-month return for the S&P 500 Index is positive (negative).

- 6-1-1 Momentum: Hold SPY (cash) when the past 6-month return, with a skip-month, for the S&P 500 Index is positive (negative).

- 100 Monthly Coin Flippers: Hold SPY (cash) when the coin comes up heads (tails).

The chart below from the report (Chart 2.) plots the relative returns to each strategy over the period studied. Gratifyingly (but not unexpectedly given our prior tests), the simple 6-month price momentum timing system (green line) is most effective, delivering 138% of cumulative outperformance over the period (Source: CXO paper). The simple 10-month moving average system (orange line) is almost as effective. The many blue lines represent 100 trials of monthly coin flipping; it is easy to see that most of the blue lines lie above the black line near the bottom, which is the return to Buy and Hold.

Chart 2. Simple Strategy Cumulative Returns Comparison

Source: CXO Advisory Group

Do Timing Strategies Work in Bull Market Periods Too?

While we would intuitively expect timing systems to add value during bear market periods, and in fact we can see that a dart-throwing monkey would probably outperform in bear markets with a coin-flip strategy, investors need a system that is reliable during bull markets too.

We set out to test 4 of the systems described in the CXO study on U.S. stocks during the period 1982 through 1999. This period represents the most consistent and powerful bull market in U.S. stocks of the past 140 years in terms of both duration and aggregate returns. If a timing system can add value during this type of bull market, in addition to adding value during difficult bear market periods, we can be much more confident of its efficacy in the future.

Chart 3. shows the total returns to a buy and hold strategy over the test period. You can see that stocks delivered a total return of 17.7%, and with a maximum drop in portfolio value from any peak to trough of 26% (all results are as of the end of the month). A buy and hold investor was never underwater for more than 20 months during this period. This compares very favorably with the period 1999 – 2009 where a buy and hold investor was underwater for 73 months during the “Tech Wreck”, and remains underwater still from the 2008 crash (Chart 1.). The annualized monthly volatility of returns was 10.7% during the 1982 - 1999 bull market period (note that daily volatility was closer to 14% over this period, but the monthly data is sufficient for comparison).

While we would intuitively expect timing systems to add value during bear market periods, and in fact we can see that a dart-throwing monkey would probably outperform in bear markets with a coin-flip strategy, investors need a system that is reliable during bull markets too.

We set out to test 4 of the systems described in the CXO study on U.S. stocks during the period 1982 through 1999. This period represents the most consistent and powerful bull market in U.S. stocks of the past 140 years in terms of both duration and aggregate returns. If a timing system can add value during this type of bull market, in addition to adding value during difficult bear market periods, we can be much more confident of its efficacy in the future.

Chart 3. shows the total returns to a buy and hold strategy over the test period. You can see that stocks delivered a total return of 17.7%, and with a maximum drop in portfolio value from any peak to trough of 26% (all results are as of the end of the month). A buy and hold investor was never underwater for more than 20 months during this period. This compares very favorably with the period 1999 – 2009 where a buy and hold investor was underwater for 73 months during the “Tech Wreck”, and remains underwater still from the 2008 crash (Chart 1.). The annualized monthly volatility of returns was 10.7% during the 1982 - 1999 bull market period (note that daily volatility was closer to 14% over this period, but the monthly data is sufficient for comparison).

Chart 3. S&P500 Total Return Dec. 1981 through Dec. 1999

Source: Shiller (2011)

The Bull Market Test

With these types of returns, a timing system has its work cut out for it. Let's see how 3 of the timing systems above stack up when markets are rising, rather than falling or moving sideways. Note that all of the tests below account for trading costs of 0.25% per trade to make the comparison more realistic.

With these types of returns, a timing system has its work cut out for it. Let's see how 3 of the timing systems above stack up when markets are rising, rather than falling or moving sideways. Note that all of the tests below account for trading costs of 0.25% per trade to make the comparison more realistic.

Table 1. Timing versus Buy and Hold in a Bull Market

Source: Shiller (2011), Butler|Philbrick & Associates

The table requires some explanation. First, the columns:

- Annualized return - simply the annualized compound return to each strategy over the time period

- Volatility - annualized monthly standard deviation, a traditional measure of risk

- Maximum Drawdown - another measure of risk that is simply the largest percentage drop from any peak in portfolio value along the way

- Randomized Annual Return - our testing software randomizes the order of monthly returns, and the signals generated by each system, to provide a more robust estimate of the worst likely average returns over the period

- Randomized Max Drawdown - similar to randomized returns, this is the worst probable drawdown that resulted from many randomly ordered monthly series, and provides a more robust estimate of true risk

- Randomized Return / Randomized Drawdown - a more robust measure of risk-adjusted returns; higher values are better

As our test used a very specific start and end date, and necessarily represents just one of an almost infinite number of possible monthly return histories, we prefer to analyze the value of any strategy based on a randomized sample of many possible return paths (in this case 2000), rather than just the one that we lived through. The "Randomized Return / Randomized Drawdown" measure provides a much more robust way for us to evaluate the effectiveness of each strategy.

On this measure, we can see that the strategy of holding an equal amount of stocks and cash, and rebalancing back to even on a monthly basis, provided the best risk-adjusted return over the duration of this bull market. It is worth noting however that the annualized return to cash from 1982 - 1999 was over 7% per year, while cash currently yields less than 1%, so it is difficult to draw any conclusions about future returns from this analysis. Further, this balanced strategy delivered absolute returns of less than 13% per year versus 17.7% for buy and hold.

Of greater consequence, both the 10-month moving average and 6-Month Momentum strategies substantially outperformed buy and hold on a risk adjusted basis, according to the more robust randomized measure (far right column in Table 1.). While buy and hold delivered slightly higher returns after trading costs during the period (17.7% versus 16.1% for 10-Month MA and 17% for 6-Month Momentum), the timing strategies realized almost a 50% reduction in maximum drawdown. Further, the randomized annual return was higher for the 6-Month Momentum strategy, indicating that from a probability weighted perspective, 6-Month Momentum timing is more likely to deliver higher absolute returns than buy and hold.

Conclusion

We saw in prior posts (here and here), and from the CXO study above that a timing system can deliver much better returns to investors when markets move sideways or down over many years. This study aimed to test these systems against a period of prolonged market strength. The value of the timing systems would be called into question if they performed much worse during long-term bull markets, as an investor would not know in advance if future returns are going to be sideways, up or down for many years.

Our study demonstrates that simple timing systems can deliver substantial risk-adjusted value to investors, even during periods of very strong bull markets. The timing systems reduced portfolio volatility by approximately 20%, and reduced month-end portfolio drawdowns by almost 50%, which makes for a much smoother experience for investors, and many less sleepless nights. Further, absolute returns were comparable even after accounting for trading costs.

Given that simple systematic investment strategies can deliver much better results during bear markets, and better risk-adjusted results during bull markets, it is difficult to imagine why any small investor would not apply a timing system to improve their chances for long-term investing success.

On this measure, we can see that the strategy of holding an equal amount of stocks and cash, and rebalancing back to even on a monthly basis, provided the best risk-adjusted return over the duration of this bull market. It is worth noting however that the annualized return to cash from 1982 - 1999 was over 7% per year, while cash currently yields less than 1%, so it is difficult to draw any conclusions about future returns from this analysis. Further, this balanced strategy delivered absolute returns of less than 13% per year versus 17.7% for buy and hold.

Of greater consequence, both the 10-month moving average and 6-Month Momentum strategies substantially outperformed buy and hold on a risk adjusted basis, according to the more robust randomized measure (far right column in Table 1.). While buy and hold delivered slightly higher returns after trading costs during the period (17.7% versus 16.1% for 10-Month MA and 17% for 6-Month Momentum), the timing strategies realized almost a 50% reduction in maximum drawdown. Further, the randomized annual return was higher for the 6-Month Momentum strategy, indicating that from a probability weighted perspective, 6-Month Momentum timing is more likely to deliver higher absolute returns than buy and hold.

Conclusion

We saw in prior posts (here and here), and from the CXO study above that a timing system can deliver much better returns to investors when markets move sideways or down over many years. This study aimed to test these systems against a period of prolonged market strength. The value of the timing systems would be called into question if they performed much worse during long-term bull markets, as an investor would not know in advance if future returns are going to be sideways, up or down for many years.

Our study demonstrates that simple timing systems can deliver substantial risk-adjusted value to investors, even during periods of very strong bull markets. The timing systems reduced portfolio volatility by approximately 20%, and reduced month-end portfolio drawdowns by almost 50%, which makes for a much smoother experience for investors, and many less sleepless nights. Further, absolute returns were comparable even after accounting for trading costs.

Given that simple systematic investment strategies can deliver much better results during bear markets, and better risk-adjusted results during bull markets, it is difficult to imagine why any small investor would not apply a timing system to improve their chances for long-term investing success.

Chart 4. Equal Weight S&P500 and cash, with monthly rebalancing.

Source: Shiller (2011), Butler|Philbrick & Associates

Chart 5. 10-Month SMA: Own the S&P500 when the index closes any month above a simple 10-month moving average; hold cash otherwise.

Source: Shiller (2011), Butler|Philbrick & Associates

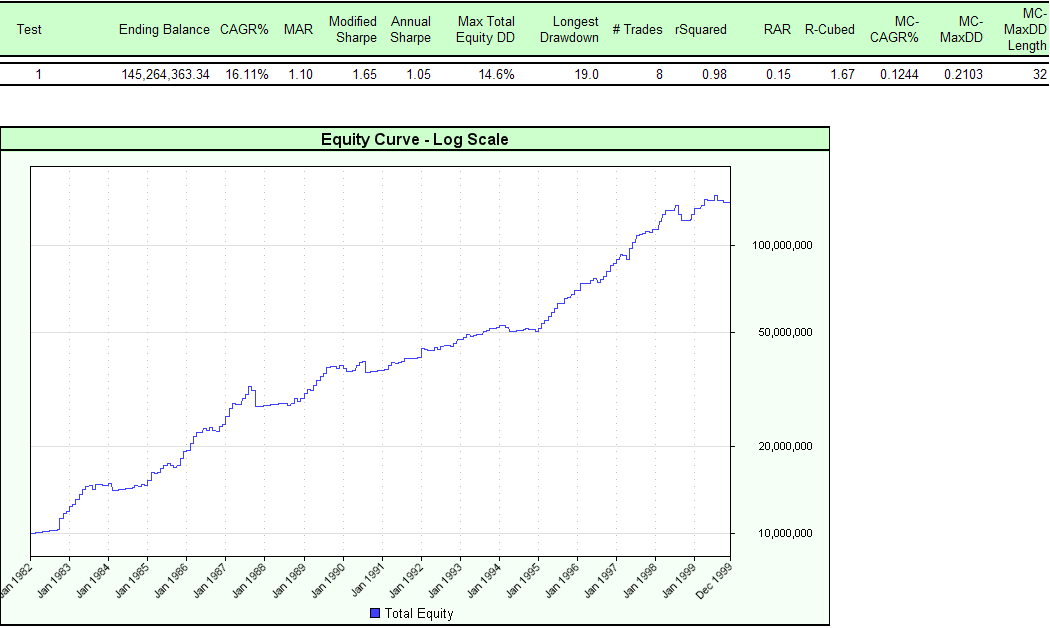

Chart 6. 6-1 Momentum: Own the S&P500 when the index delivers 6 month price performance above the 6 month return to cash; hold cash otherwise

Source: Shiller (2011), Butler|Philbrick & Associates

Source: Shiller (2011), Butler|Philbrick & Associates