As usual, you are the butt of the joke.

Everywhere you turn, you are bombarded with 1, 3, and 5 year track records for investment products. The investment management industry knows that you are influenced by percent symbols preceded by large numbers, so they market products with the best 1, 3 and 5 year track records, prominently featuring them in newspaper and TV advertisements, knowing that you will be unable to resist the urge to chase into those funds to avoid missing another year of riches.

Unfortunately, as you probably surmised, this almost never works out. The products with the best track records over the past few years are not the products that deliver the best track records in subsequent years. In fact, there is strong evidence that chasing managers with strong 3 and 5 year track records is actually harmful to your portfolio health. This article will explore the evidence against using a 3 to 5 year track record to make investment decisions, and point to some alternative solutions.

3 Year Track Records Are for Suckers

The most commonly cited study of actual retail investor behaviour is the Dalbar Quantitative Analysis of Investor Behaviour which summarizes findings about mutual fund investor behaviour over the past 20 years. We plucked two important, and we think related, facts from the piece and summarized them in charts 1 and 2 below. Chart 1. shows the average holding period for each class of mutual fund (stocks, bonds and balanced funds), and Chart 2. shows the realized returns to actual investors on their stock and bond mutual fund holdings, over the period 1991 - 2011.

Chart 1. Stock and bond investors hold funds for 3 years; balanced investors give it one more year

Source: Dalbar, 2012

Chart 2. Actual results to mutual fund investors vs. stock and bond benchmarks - 1991 to 2011

Source: Dalbar

From Chart 1. we can see that, on average, retail investors go chasing into new 'hot funds' about every 3 years or so; balanced investors seem to hang on a little longer, for reasons we explored in this article. Chart 2. highlights the insanity of this approach. Equity investors earned 4% per year less than the large cap stock benchmark over the same period, while bond investors fared even worse. Sure, about half of the decay can be attributed to fees and taxes, and a portion to bad market timing (strangely we didn't receive any calls from investors in a panic to buy in early 2009), but a measurable portion of the lag is due to misguided product selection on the basis of three year track records.

Chart 3., from the annual SPIVA report on active manager performance (2011 version) demonstrates the tendency for managers who demonstrate top quartile performance over a 5 year period to fall out of the top quartile over the next 5 years. One might randomly expect 25% of the managers who rank in the top quartile in the first 5 years to again rank in the top quartile during the second period. In fact, just 6% of these managers actually persist in the top quartile, implying a very substantial reversion to the mean effect.

Chart 3. Mutual fund manager performance persistence over 5 year periods

Source: SPIVA (2012)

Chart 4. shows that institutions act largely on the same schedule as retail investors, with manager termination decisions based largely on 3 to 5 year trailing results. This is not surprising because institutions are run by humans too.

Chart 4. Average evaluation period for manager termination by pension funds

Source: Employee Benefit Research Institute

Chart 5. clearly illustrates the impact of this phenomenon in the pension space. The grey bars represent the average annualized performance of terminated managers in the three years prior to, and three years subsequent to, their termination. The white bars represent the performance of replacement managers in the same years. Clearly institutions are hiring managers with exceptional historical track records over trailing 3 year periods, and firing managers with poor track records. The joke is on the institutions, however, since on average the fired managers go on to outperform the hired managers over the subsequent 1, 2, and 3 year periods!

Chart 5. Excess returns to terminated and newly hired managers in the 3 years prior to, and subsequent to, termination

What an incredibly frustrating reality for retail and institutional investors alike. How can it be that managers with the best track records over as long as 5 years don't work out to be great investments in subsequent years? Does a track record mean anything? For the most part, we don't think so.

Manager Skill, or Factors in Drag?

It is important to remember that most investment managers are human beings. (I say 'most' because a minuscule but growing portion of managers are actually computers). As such, most managers are really just overconfident, incoherent collections of habits, assumptions, ideologies, and cognitive and emotional biases emanating from the most dangerous black-box of all - the human mind. Sometimes these habits, assumptions and biases are aligned with the market, and the manager does well. Sometimes the manager is 'out of sync', and he does poorly.

In reality, it is better to think of managers as inconsistent conduits to somewhat persistent factors that manifest in markets from time to time to drive outperformance from a certain investment approach. In the equity space, academics suggest that 4 factors explain the majority of long-term stockpicking performance. One might infer that the success or failure of most managers over any period of 3 to 5 years largely depends on whether the manager's biases were aligned with one of the following factors that happened to also be working over the same period.

- Market factor: this is commonly referred to as beta, and refers to the fact that most stocks tend to move in the same direction as the index

- Small-cap factor: it has long been recognized that small-cap stocks outperform large-cap stocks over the long-term

- Value factor: cheap stocks tend to outperform expensive stocks over the long term

- Momentum factor: stocks that have gone up over the past 1 to 12 months tend to outperform over the long term

Recently, academics and practitioners have reluctantly added a low volatility (or low beta) factor to explain the observed outperformance of low volatility stock portfolios, and we will include this factor in our analyses below.

Chart 6. offers graphical evidence of the value and momentum effect within large-capitalization stocks. Specifically, the chart demonstrates how a strategy of rotating into the strongest stocks every month, and a strategy of rotating into the cheapest stocks every year, have outperformed a strategy of holding the broad stock market index since 1927.

Chart 6. U.S. large capitalization stock market value and momentum factor tilt portfolios

Source: Ken French database

It is our assertion that clients should be much less concerned with the track records of individual managers, and much more concerned with the performance of a manager's style factor. If you can identify what factors (or what mix of factors) is most likely to generate the strongest risk-adjusted returns over your rebalance horizon, this information is of much greater value than identifying which managers might outperform their style benchmarks.

If 96% of mutual fund performance is explained by style factors, and most managers underperform the market and their style benchmarks, then investors should concentrate on allocating to factors, not managers. In the real world, when the value factor is outperforming, value biased managers will be high-fiving each other at the water cooler and celebrating their unique and robust stock-picking talent. Growth (or anti-value) managers, meanwhile, will be crying in their beer and lamenting the 'broken' market that isn't cooperating with their investment bias. Chart 7. clearly illustrates this effect, as value managers outperformed for the first four years of the last decade, gaining 26% vs. their growth oriented peers by late 2006.

Chart 7. Value vs. Growth: Luck or Skill?

Source: Stockcharts.com

However, just as value managers were buying their Porsches and brownstones in 2006, their performance streak ended. Over the next 6 years, value managers endured a steady diet of crow while their growth brethren feasted on rich returns. Chart 8. illustrates the same phenomenon for managers with small vs. large-cap biases over a 20 year horizon, but the same effect plays out in all factors: dividend stocks, momentum stocks, low volatility stocks, etc.

Chart 8. Small cap vs. Large Cap: Luck or Skill?

Source: Stockcharts.com

If style factors explain 96% of equity manager performance, and a single factor can deliver 25% - 50% or more of outperformance over a four year period, you can see that the decision to allocate to either value or growth, small-cap or large-cap (insert any factor here) completely dominates the decision about which specific value, growth, small-cap or big-cap manager to use.

Surely Buffet is a Special Case, Right? Wrong.

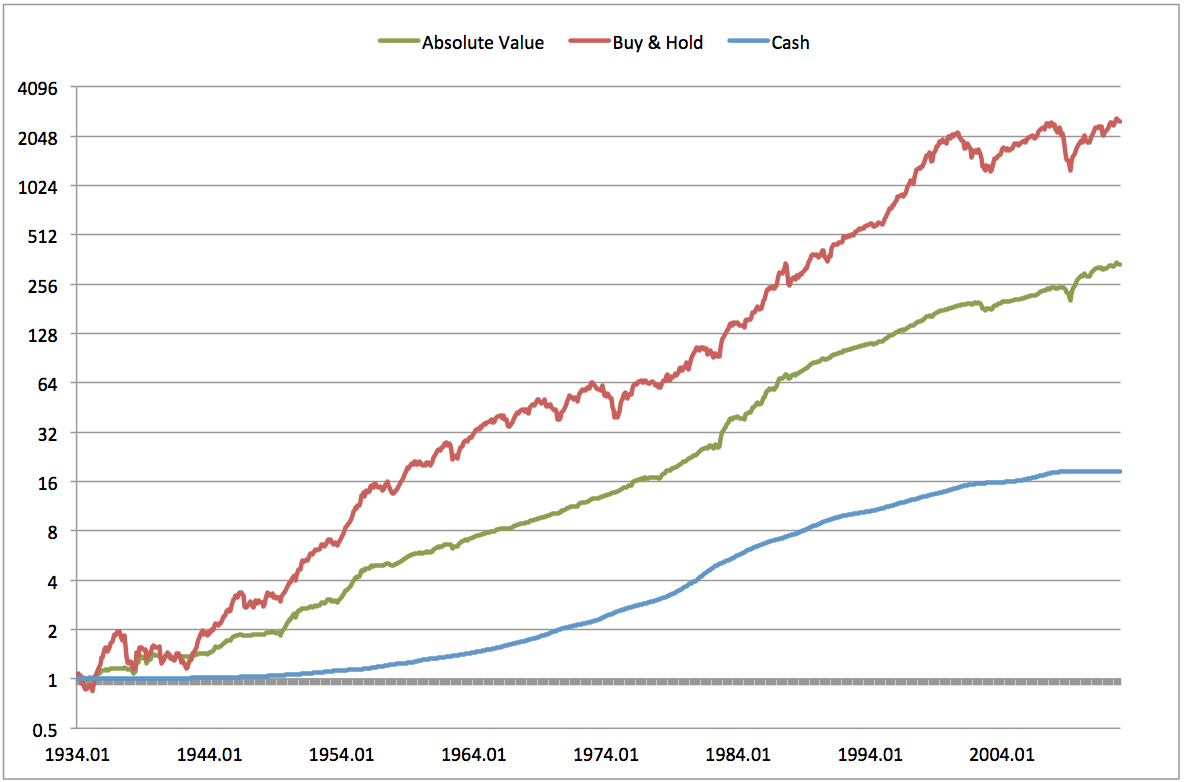

Interestingly, a group at Yale investigated the full trading history of Warren Buffet's investment vehicle, Berkshire Hathaway to discover whether and which systematic factor exposures can effectively explain the seeming miraculous long-term outperformance Buffett has delivered over the years. The authors regressed the monthly returns to Buffet's portfolio (assembled through 13F filings) against the same 5 factors plus another factor, 'Quality', as defined in Asness, Frazzini, and Pedersen (2012b). They discovered that Buffet's strategy was essentially to purchase low beta, high quality stocks (using the long held academic definitions), and lever his portfolio by 60%. The authors regressed Buffet's returns against their 6 factors and then simulated the growth of the equivalent factor portfolio (green line) over Buffet's full investment horizon and compared it to Buffet's actual performance (blue line). The results are in chart 9. below.

Chart 9.

Regarding the ability of factors to explain away Buffet's magical performance streak, the Yale authors suggest:

We see that Berkshire loads significantly on the [low beta] and [quality] factors, reflecting that Buffett likes to buy safe, high-quality stocks. Controlling for these factors drives the alpha of Berkshire’s public stock portfolio down to a statistically insignificant annualized 0.1%, meaning that these factors almost completely explain the performance of Buffett’s public portfolio.

Style Boxes Are Silly

The small-cap and value factors form an integral framework for many institutions, as they are the two dimensions used in a traditional 'style box' model. Investors who are guided by this model seek to gain exposure to each 'style box' by seeking out top managers in each style.

Figure 1. Morningstar's Style Box

Source: Morningstar

In reality, this is just a misguided method of factor investing; misguided because investors just end up with what is essentially a 'market' portfolio in the end, as they own both small and big stocks, and value and growth stocks. Further, 'large cap' and 'growth' are anti-factors, which means they have tended to deliver returns below the market portfolio over the long-term. For this reason (and others that are more nuanced), the style box model should be abandoned in favour of a model that embraces true systematic factor tilts against an efficient 'market portfolio'.

Should We Buy Strong Factors?

We've learned that we should be thinking about allocating to factors instead of managers because managers are just inconsistent factors in drag with a strong propensity to underperform. But how should we think about allocating to factors?

We tested a strategy of rotating into the strongest and weakest factors quarterly based on trailing 1, 3, and 5 year performance to see if any of these approaches work any better than holding an equal-weight portfolio of factor tilts, rebalanced quarterly.

Table 1. Summary of factor rotation strategies

Source: Ken French database, Standard & Poor's, Yahoo finance

We've highlighted the worst performing strategies in red. You can see that a strategy of allocating to the factor that performed the best over the past 3 and 5 year periods delivered the worst absolute and risk-adjusted performance over our sample period (1995 - 2012). In fact, the best approaches would have been to allocate to factors that delivered the worst performance over either the past 1 or 5 years, or to allocate equally to the best and worst factors over the prior 1 year period. A strategy of allocating equally to all factors and rebalancing quarterly delivered similar risk-adjusted returns, but lower absolute returns.

From the table above, we would conclude that there is a weak mean-reversion effect with equity market factors over 1 year and 5 years, and an even weaker momentum effect over a 1 year horizon. Clearly the worst strategies are the ones that are embraced by most investors: buying the strongest performing approach over the past 3 to 5 year period.

Future Directions

From a statistical standpoint, factors don't appear to exhibit either a meaningful momentum or mean reversion signal, so investors really don't have much hope of excess returns from chasing into managers with great track records or backing up the truck on managers with awful track records.

However, both of these dynamics really come down to estimating which factor(s) will deliver the highest returns. If we take the perspective that simple performance offers no meaningful information about future returns, then we are left with optimization alternatives related to relative volatility, such as risk parity, or the covariance matrix, such as minimum variance. We explore these approaches at length in our paper, 'Portfolio Optimization with Factor Tilts', but here is a sneak peak.

Chart 10. 5 Equity Factors, Minimum Variance, Rebalanced Monthly, 25% Filter, Portfolio Target Volatility (1%), Max 100% Exposure

Source: Ken French database, Standard & Poor’s, Yahoo Finance

Chart 11. 5 Equity Factors, Minimum Variance, Rebalanced Monthly, 25% Filter, Portfolio Target Volatility (1% daily), Max 200% Exposure

Source: Ken French database, Standard & Poor’s, Yahoo Finance

Mutual fund companies and institutional consultants will continue to feed your biases by advertising their best track records, but you don't have to fall for it. With a little research - and an open mind - you can uncover novel methods based on academically validated principles with a proven history of delivering market-beating returns with lower risk.

In our opinion, the most interesting and prospective extension of the concepts discussed above are in the form of Tactical Alpha rather than traditional security selection. This type of approach deals with the allocation of factors across multiple asset classes (see here from AQR[registration required] and here for our own paper), which allows for many more sources of return and diversification, which gets us much closer to investment Nirvana.

Source: (Brooks & Gray, 2003)

Source: (Brooks & Gray, 2003) Source: (Brooks & Gray, 2003)

Source: (Brooks & Gray, 2003)